EUAs cautiously inched up on positive conflict developments

The easing power demand, rising wind production and decreasing gas prices continued to pressure the power spot prices yesterday which averaged 240.80€/MWh in Germany, France,…

rocket domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /home/befikry/energyscan.befikry.com/wp-includes/functions.php on line 6121

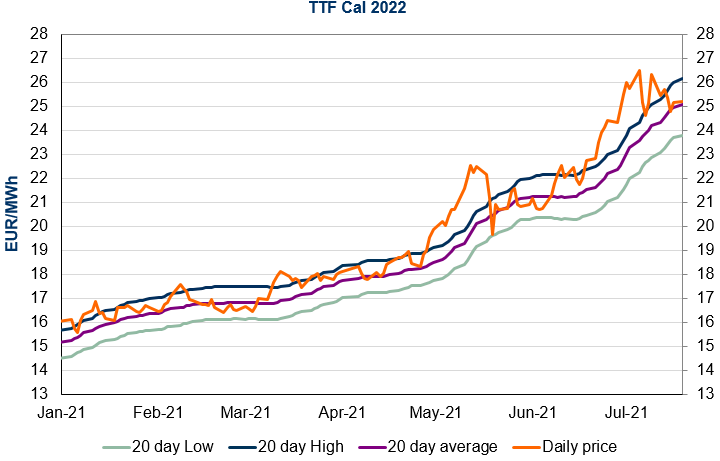

European gas prices extended gains yesterday, supported by rising temperatures, ongoing weak supply and strong Asia JKM prices (+2.59% on the spot, to €41.291/MWh). On the pipeline supply side, Russian flows remained stable at 163 mm cm/day on average yesterday, with the Nord Stream 1 gas pipeline still shut for a 10-day planned maintenance that started on 13 July. Norwegian flows were up, averaging 331 mm cm/day, compared to 326 mm cm/day on Friday.

At the close, NBP ICE August 2021 prices increased by 2.900 p/th day-on-day (+3.39%), to 88.380 p/th. TTF ICE August 2021 prices were up by 81 euro cents (+2.32%) at the close, to €35.649/MWh. On the far curve, TTF Cal 2022 prices were up by 4 euro cents (+0.16%), closing at €25.194/MWh.

Weak supply and strong Asia JKM prices could continue to lend support to European gas prices today. However, after yesterday’s increase, profit taking and technical resistances (€36.011/MWh on TTF August 2021 and €25.462/MWh on TTF Cal 2022) could contribute to exert downward pressure.